04 / Fraud

Transactional Fraud Analytics ft. Mastercard

Worked with Mastercard's fraud analytics team to redesign the real-time risk scoring pipeline for a specific transaction corridor showing elevated anomaly rates.

Company

Mastercard x BOLT UBC Datathon

Role

Datathon Participant

Year

Mar – Apr 2024

Tags

01 / Role & Scope

Scope

Led a small team in Mastercard's case competition. I owned the analytical approach, directed the clustering and classification work, and built the strategy we presented to stakeholders.

02 / Problem

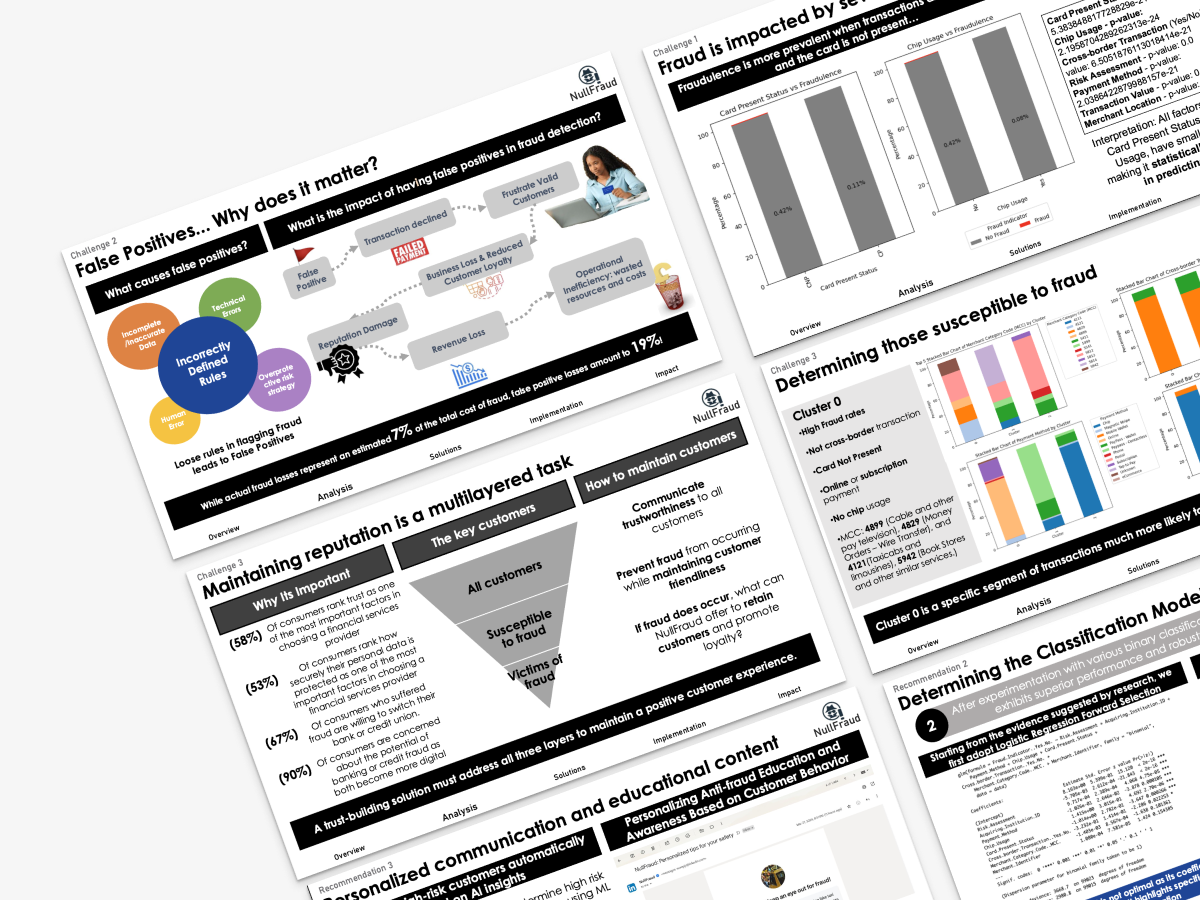

The Real Cost

The fictional bank we were analyzing had a fraud cost problem, but not the one most people would focus on. Actual fraud accounted for 7% of total fraud-related losses. False positives accounted for 19%. The bank was losing nearly three times more money from wrongly declining legitimate customers than from fraud itself. And every false decline erodes trust, drives churn, and quietly damages the brand in ways that don't show up in a fraud report.

03 / Solution

SPArk

Most teams in a competition like this jump straight to "build a better fraud classifier." We went upstream. Before trying to predict fraud more accurately, I wanted to understand who was actually getting caught in the false positive net and why.

We ran KMeans and KModes clustering across the transaction data and isolated a segment we called Cluster 0: customers with a 42.6 basis point fraud rate whose transactions were entirely domestic, card-not-present, concentrated in online payments with zero chip usage. The fraud was spiking in specific merchant categories like cable services, wire transfers, taxis, and bookstores. Once we could see the shape of the problem that clearly, the solution became much more targeted.

We built a three-part strategy called SPArk. EMV payment tokenization to protect primary account numbers at the system level. A Random Forest binary classifier (90.5% accuracy) to replace the bank's blunt legacy rules that were generating most of the false positives. And a real-time SMS confirmation flow so the bank could verify suspicious transactions with the customer instead of just declining the card and hoping for the best.

We walked stakeholders through the full experience using a persona named Suzie to show how each layer of the strategy would work in a real transaction, from the moment a purchase looks suspicious to the moment it's resolved.

04 / Result

What Shipped

Projected savings of $12,000 per 100,000 transactions while maintaining customer trust and reducing the false positive rate that was costing the bank nearly 3x more than actual fraud.

Next Project

05 / Analytics